Introduction: a Market transformed

Doing business in Russia has become one of the most contested strategic questions in international commerce. Since 2022, geopolitical tensions, sanctions, and economic fragmentation have fundamentally altered operating conditions for foreign companies. Many have been forced to reconsider whether — and how — they can remain active in the market.

And yet, despite these pressures, many global players have not left. This paradox — high geopolitical risk coexisting with persistent business activity — raises a question that is both practical and strategic. Is Russia still a viable market for international companies? Recent evidence suggests the answer is not binary. Russia is no longer a conventional growth market. Neither can it be written off entirely.

A resilient but transformed market

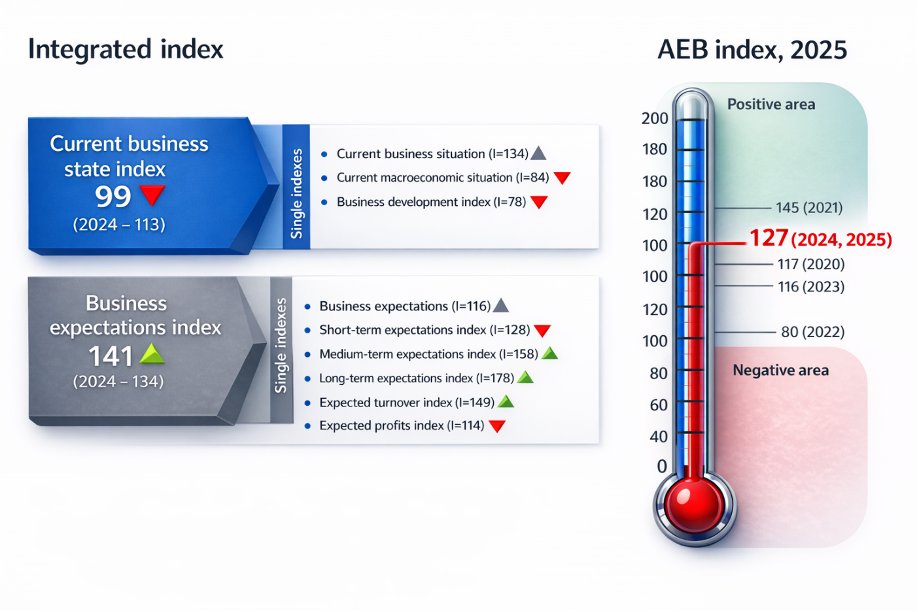

Contrary to expectations following the 2022 shock, the Russian economy has retained a significant degree of resilience. According to the AEB Business Climate Survey 2025, more than 56% of companies reported higher turnover in 2024. This signals a measurable recovery in overall business activity. The AEB Business Climate Index reached 127 points out of 200 — a steady improvement since falling to 80 in 2022. Long-term expectations have also strengthened. 82% of respondents anticipate significant growth over the next decade, up from 66% the previous year.

The AEB Index is based on interviews with 100 companies conducted between April and May 2025. The integrated index uses a 0–200 scale. It combines sub-indexes reflecting current business conditions and future expectations. Higher values indicate a more positive business assessment.

However, this resilience conceals a structural reality. The Russian business environment has not reverted to pre-2022 conditions. It has undergone a permanent structural change.

From global integration to local adaptation

One of the most significant shifts concerns how companies operate internally. According to the FIAC–B1 Group survey, 95% of firms now rely on local management for decision-making. Only a marginal share remains fully controlled by foreign headquarters. This points to a broader process of localisation under constraint. Faced with geopolitical pressures and operational restrictions, firms have adjusted in three ways. They have delegated authority to local management, have relocated key functions to Russian subsidiaries and have reduced reliance on global headquarters.

Why localisation is also strategic

This shift is not merely operational. It is also strategic. Greater local control enables firms to navigate sanctions more effectively, maintain market access, and reduce political exposure.

Sanctions, barriers, and structural constraints

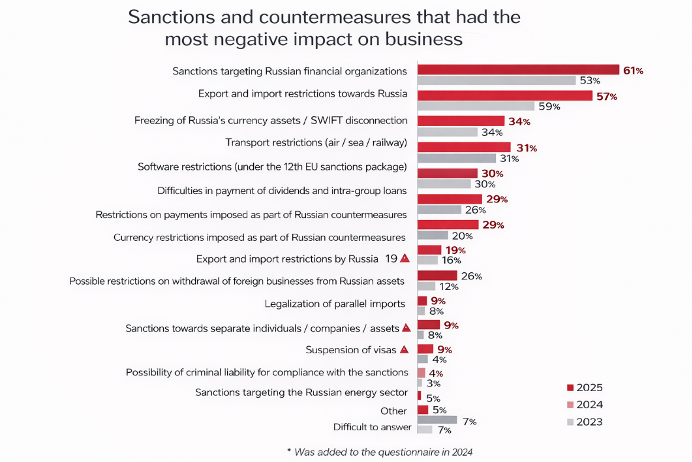

Despite signs of resilience, the Russian business environment remains heavily constrained. 87% of companies report having been negatively affected by Western sanctions and Russian countermeasures. The main obstacles include financial restrictions – particularly disconnection from SWIFT – as well as trade limitations and disruptions in transport and logistics. Additional challenges include difficulties in payments and settlements, reputational exposure, and the refusal of foreign partners to engage with Russia-linked entities.

Doing business in Russia: no longer a normal market

These developments point to a central conclusion. Russia can no longer be understood as a normal market. It has become a politically conditioned business environment. Commercial decisions now depend on geopolitical risk in a way they did not before 2022.

The risk paradox: high uncertainty, persistent presence

Here lies the central paradox: a considerable share of companies have not exited the market. According to AEB data, 67% of firms do not plan to close their Russian operations. FIAC data indicates that 92% of companies consider their Russian business to be successful. Elevated risk does not automatically translate into market withdrawal. Many firms continue to operate on the basis that Russia still offers tangible commercial value.

Several factors explain this pattern. Russia remains a large domestic market. The departure of many Western competitors has reduced competitive pressure. It has also created openings for firms that stay. Companies have identified new prospects — entry into new market segments, increased market share, and broader business growth within Russia.

Operational constraints: logistics, technology, and labour

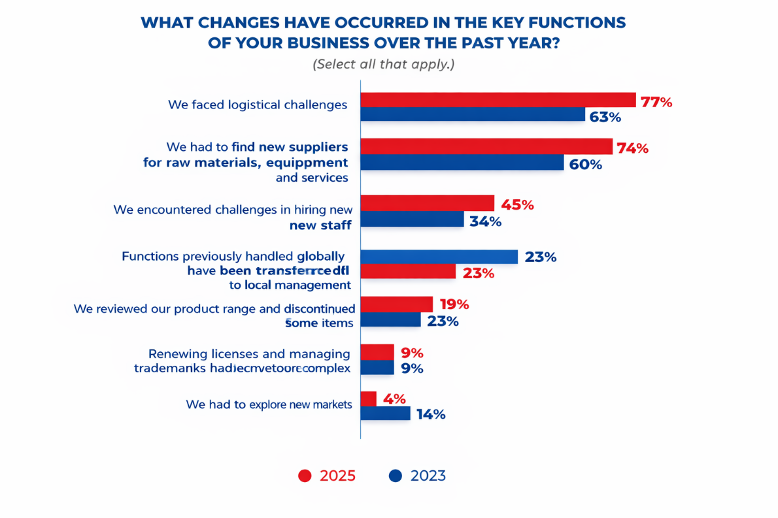

Although companies continue to operate in Russia, practical conditions have grown markedly more complex. A set of interconnected operational constraints now affects supply, labour, and technology.

Logistics and supply chains represent the most pressing challenge. Around 77% of companies report difficulties in this area, up from 63% in 2023. Procurement of equipment and essential inputs has become progressively harder.

Technology constitutes a further area of constraint. Access to global technologies remains possible to some extent. It is, however, increasingly limited. Companies have responded by turning to local substitutes, strengthening ties with Asian partners, and investing in in-house development.

Risk perceptions are moderating

Perceptions of risk appear to have moderated over time. According to FIAC data, 77% of companies still assess the level of risk as above average. This represents a decline from 85% in 2023. Firms are progressively adapting. Geopolitical risk is increasingly absorbed into routine strategic and operational calculations rather than treated as an exceptional shock.

Long-term outlook: isolation or opportunity?

The long-term outlook remains ambivalent, but it is not negative. According to AEB data, 82% of companies expect economic growth over a six- to ten-year horizon. Moreover, 46% of firms are considering new investments in Russia or the broader Eurasian region. For many companies, Russia is no longer a short-term commercial opportunity. It has become a long-term strategic bet — a market shaped simultaneously by isolation, adaptation, and selective opportunity.

Implications for businesses: five key lessons

Doing business in Russia offers important lessons for firms operating in geopolitically sensitive environments.

First, geopolitical risk must now be treated as a structural variable, not a temporary external shock. Firms can no longer treat it as an exogenous disruption. It must be integrated into core strategic decision-making.

Second, localisation has emerged as a key survival strategy. Greater reliance on decentralised decision-making and local management structures can help firms preserve operational continuity under conditions of uncertainty.

Third, resilience has become at least as important as efficiency. In politically fragmented environments, redundant supply chains, alternative partners, and adaptive operational structures are no longer optional. They are essential.

Fourth, continued market presence may create strategic advantages. Firms remaining active in high-risk markets may be better positioned to capture market share. This is especially true where competitor withdrawal has created new openings.

Fifth, reputation management has become critical. Operating in politically sensitive contexts exposes firms to regulatory and operational risks. It also generates significant reputational pressure at the global level.

Conclusion

The central lesson is clear. Geopolitical risk does not eliminate business opportunities. It transforms their nature. For firms willing and able to adapt, doing business in Russia continues to offer selective opportunities. Success depends on one capacity above all: the ability to balance risk and opportunity, global strategy and local adaptation, efficiency and resilience.

In this sense, Russia is not merely a case study. It is also an early indicator of how international business may increasingly operate in a world defined by fragmentation, political tension, and strategic decoupling.

May 2, 2026

You may also enjoy reading…