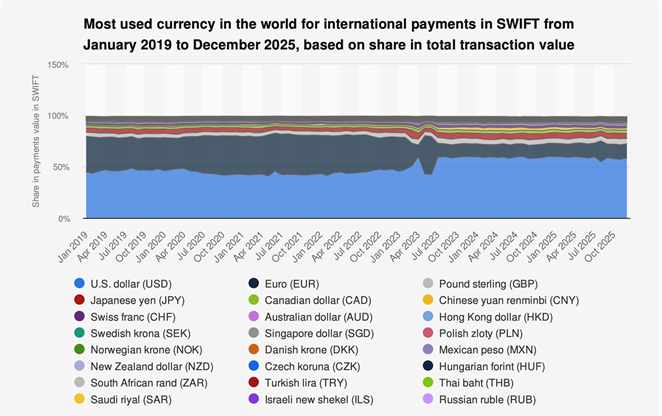

US, China and the petrodollar system sit at the intersection of geopolitics and financial power — a never-ending story that defines the global power scenario of the 21st century. Financial superiority has become an increasingly decisive realm of this contest. If we take a snapshot of the current state of the two currencies — dollar and renminbi — the picture is clear: the global transaction world remains US-dominated. The dollar accounts for more than 50% of payments value in SWIFT. On the other side, renminbi usage almost doubled, moving from 1.24% of global transactions in January 2019 to 2.13% in October 2025. The renminbi’s presence remains marginal — but it is growing.

That tension — between stability at the core and change at the periphery — frames the broader question. If global payments still run on dollars, why does the renminbi gain traction at all?

This article examines the geopolitical and financial frictions between the US and China. It analyses the current status quo, the rationale behind the persistence of the petrodollar, and China’s evolving strategy.

The Dollar’s Structural Dominance

To frame the broader picture, consider the dollar’s current footprint. It accounts for around 85% of foreign exchange transactions and nearly 60% of global foreign exchange reserves. Global trade follows the same pattern. The renminbi, by contrast, operates in the low single digits.

The two countries also diverge sharply in their structural roles. China is the world’s largest oil importer and plays a crucial role in global trade, manufacturing, and energy investment. A clear structural asymmetry emerges: China is systemically central in trade, yet marginal in currency. This discrepancy is not new — but it grows harder to ignore, especially as the recent conflict involving Iran tightens oil supplies and pressures the whole system.

Historically, economic size and currency dominance have converged, albeit with long lags. The dollar’s persistence — despite the relative decline of US weight in certain areas — reflects not just economic fundamentals but the deep inertia of the existing system. The result is a world that is still overwhelmingly dollar-based, but no longer perfectly aligned with the actual distribution of global economic power.

The Petrodollar: Institutional Origins

The dollar’s dominance does not rest on economic power alone. An institutional framework built in the 1970s underpins it. Following the breakdown of the Bretton Woods system, the US secured agreements with oil producers — most importantly Saudi Arabia — to denominate oil trades in dollars.

This decision anchored the dollar at the core of global trade. Oil is the most traded commodity on the planet. By pricing it in dollars, countries importing oil needed to hold dollars, which created structural and persistent demand for the currency. Oil exporters, in turn, recycled their dollar revenues into US financial assets — particularly US Treasuries. This reinforced the dollar’s role as a store of value and expanded US capital markets.

The Self-Reinforcing Loop

What emerged was a self-reinforcing system. Trade generated demand for dollars. That demand sustained deep financial markets. Those markets strengthened the incentive to keep using the dollar. Over time, this circular dynamic produced strong inertia.

After a currency achieves dominance, it accumulates network externalities. The more actors use it, the more convenient it becomes to keep using it. Alternatives face higher transaction costs, exchange risks, and thinner markets. In practice, the dollar system exhibits features of a natural monopoly.

The supporting infrastructure reinforces this further. Dollar-based markets offer greater depth and liquidity than any rival, along with a wide range of safe assets. Institutional backing matters too: the Federal Reserve acts as a global lender of last resort, while the broader financial architecture — from payment systems to legal frameworks — remains dollar-centric.

The economy, therefore, changes faster than the monetary system. As global economic weight shifts, currency dominance adjusts slowly. The renminbi’s gradual ascent does not imply it will replace the dollar anytime soon.

China’s Strategy: Building a Parallel Layer

China has not chosen to confront the dollar system head-on. Instead, it works around it. Rather than seeking to displace the dollar at the heart of global finance, Beijing increases the renminbi’s role in areas where it already holds influence — trade, energy, and bilateral finance. As Bracarense and Berthonnet (2024) argue, this reflects an attempt to build a parallel monetary layer rather than a systemic replacement (doi:10.1080/00213624.2024.2307796).

Trade Settlement

The first channel is trade settlement. China has steadily expanded renminbi use in transactions with partners that are less tightly tied to the dollar economy. In energy and oil markets, more bilateral deals now settle in renminbi — particularly with Russia and Iran, where sanctions and political tensions create incentives to bypass dollar infrastructure.

Financial Infrastructure

The second channel is financial infrastructure. China introduced renminbi-denominated oil futures in Shanghai and grew offshore renminbi markets alongside bilateral currency swap lines. These moves aim to support the currency beyond simple trade invoicing. Historically, dollar-centred markets performed the role of providing liquidity, hedging instruments, and settlement alternatives. China now tries to replicate those functions.

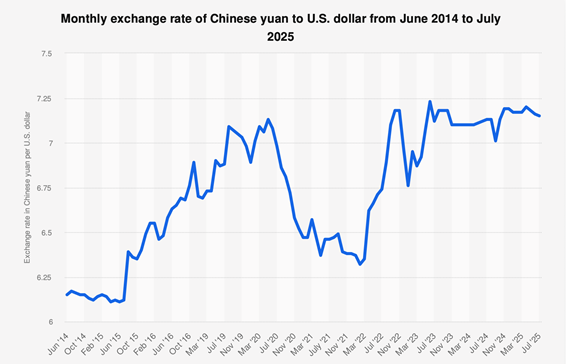

Moreover, the renminbi has gained relative stability vis-à-vis the dollar, reflecting effective policies by Chinese policymakers to limit depreciation and build credibility.

Source: Statista 2026

Resources and Finance

The third channel links resources directly to finance. Through oil-backed loans, Belt and Road Initiative (BRI) financing, and investment in both fossil and renewable energy, China expands renminbi circulation. In doing so, it replicates — in a different form — the connection between energy markets and currency demand that historically underpinned the petrodollar system.

Together, these moves do not yet constitute a systemic alternative. They point instead to a deliberate strategy: not to overturn the existing order, but to build a parallel layer within it.

Structural Drivers of Renminbi Expansion

Broader shifts in the global system now accelerate renminbi adoption — and many of these shifts originate within the dollar-based order itself.

The most significant driver is the growing use of financial sanctions. The dollar’s centrality gives the United States powerful leverage over global transactions. However, this same feature motivates targeted countries to reduce their dollar exposure. In several cases, sanctions directly accelerated the search for alternative settlement currencies, with the renminbi as the primary candidate.

Shifting Trade Geography

The geography of trade also evolves in China’s favour. South-South exchanges are growing. China’s weight as a trading partner rises. Both trends create natural incentives for counterparties to invoice transactions in renminbi — especially where strong bilateral ties with Beijing already exist.

Energy markets add further momentum. As the world’s largest oil importer, China holds both the need and the leverage to negotiate settlement terms. Its expanding role as a major investor in energy infrastructure — particularly across developing economies — further catalyses renminbi circulation.

Despite these developments, the constraints remain significant. The renminbi’s international role is still limited by structural factors that distinguish it from the dollar. Most importantly, China’s financial system is not fully open. Capital controls, limited convertibility and a high degree of state intervention reduce the attractiveness of the renminbi as a global store of value. While China has developed large financial markets, access remains more restricted and less predictable than in the United States. This affects how the currency is used. Unlike the dollar, which functions as a global, multilateral medium, the renminbi is often confined to bilateral relationships. Countries that receive payments in renminbi frequently face a choice: use it to trade with China or convert it into another currency. This constraint hinders its broader circulation.

Trust matters as well. A dominant international currency requires not only scale, but confidence in the underlying institutions. The dollar benefits from decades of established credibility, deep markets and legal predictability — features that cannot be replicated quickly. In that sense, the renminbi is expanding, but not frictionlessly.

Conclusion: Towards a Plural Configuration

Given all these considerations, the most likely outcome in the evolving landscape of US, China and the petrodollar system is not a sudden transition from dollar to renminbi, but a more gradual reconfiguration. The dollar is likely to remain dominant in the near term, supported by the depth of its markets and the inertia of existing structures. What may change is the degree of concentration. As the renminbi gains ground in specific regions or sectors — particularly where China’s economic presence is already substantial — the system could evolve toward a more plural configuration. Instead of a single hegemonic currency, multiple currencies may coexist, each dominant within its own sphere.

This would mark a shift from a unified system to a more fragmented one. The dollar would continue to anchor global finance, but with increasing competition at the margins. The renminbi, in this context, would not replace the dollar, but reshape the environment in which it operates. The dominance of the dollar remains intact. But the edges may be beginning to move.

You may also enjoy reading…