Why CIPS vs SWIFT defines the future of financial power

Behind every international wire transfer, trade invoice, and central bank operation lies a messaging infrastructure invisible to markets yet structurally decisive for geopolitical power. SWIFT — the Society for Worldwide Interbank Financial Telecommunication — has performed that function since 1973. China’s Cross-Border Interbank Payment System (CIPS), launched in 2015, is its most deliberate and consequential challenger. The contest between the two systems is not simply a technical rivalry. It is an institutional front in the broader struggle over who sets the rules of global finance.

SWIFT and the architecture of dollar dominance

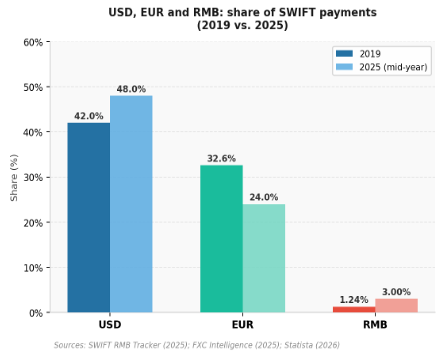

SWIFT is not a payments system. It is a secure messaging network transmitting payment instructions between financial institutions — the language through which banks coordinate the actual movement of funds. Its reach is staggering. It connects over 11,500 institutions in more than 235 countries and territories, processing approximately 44 million messages per day. It underpins an estimated $150 trillion in annual cross-border flows. The US dollar accounts for roughly 48% of SWIFT transaction value; the euro for around 24%. No other currency approaches those figures.

SWIFT’s architecture is formally cooperative and country-neutral — headquartered in Belgium and governed by a board of member institutions. Yet structural neutrality coexists with a practical reality. Most transactions flow through dollar-correspondent banking chains anchored in the United States. Washington therefore retains significant leverage over the system. That leverage became unambiguous in 2012, when Iranian banks were disconnected under US-EU sanctions. It became fully explicit again in 2022, when seven major Russian banks were expelled following the invasion of Ukraine. The ruble fell more than 30% in the immediate aftermath. An estimated $700–800 billion in annual cross-border flows were disrupted. The message to the rest of the world was unmistakable: access to SWIFT is conditionally granted, not universally assured.

CIPS: architecture and strategic intent

China conceived CIPS explicitly to reduce its exposure to this vulnerability. CIPS Co. Ltd. operates the system under the supervision of the People’s Bank of China (PBOC). It functions as a real-time gross settlement (RTGS) system for cross-border renminbi transactions. Crucially, it combines the messaging and settlement functions that SWIFT and correspondent banking handle separately. Its growth has been rapid. From 19 direct participants at launch, CIPS reached 168 direct and 1,461 indirect participants by end-2024. Institutional access now extends to nearly 5,000 entities in 185 countries. Annual transaction volume in 2024 reached ¥175 trillion (roughly $24 trillion), a 43% increase year-on-year — growth far outpacing SWIFT’s over the same period.

CIPS 2.0 and the digital yuan integration

In April 2025, China launched CIPS 2.0, integrating the digital yuan (e-CNY). The new version enables settlements completable in approximately 7.2 seconds — a significant improvement over the multi-day cycles of legacy correspondent banking. The system also forged its first direct partnerships with foreign banks in the Middle East and Africa. These are regions where dollar-dependency is increasingly a strategic liability. In March 2026, CIPS set a single-day transaction record. Average daily volume rose nearly 50% from February, partly driven by accelerating renminbi usage in oil trade amid renewed supply disruptions from the Iran conflict.

A parallel system, not a replacement

Despite this trajectory, characterising CIPS as a SWIFT replacement remains analytically premature. The most significant structural constraint is dependency. An estimated 80% of CIPS transactions still rely on SWIFT’s messaging infrastructurefor transmission between institutions not directly connected to CIPS. The two systems are, for now, more complementary than adversarial. A memorandum of understanding signed between SWIFT and CIPS underscores this, aimed at enhancing interoperability. SWIFT has also accelerated its own gpi (Global Payments Innovation) initiative in response to competitive pressure, now achieving same-day settlement on nearly 100% of transactions.

The currency constraint

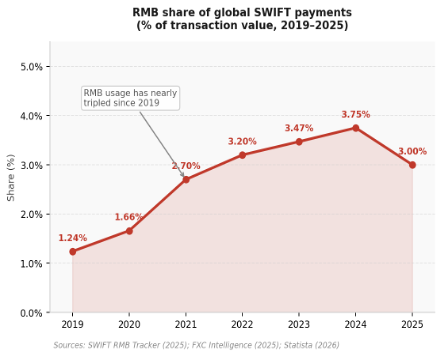

The second structural constraint is currency scope. CIPS is a renminbi-denominated system by design. The yuan accounted for approximately 3% of global SWIFT payment value in mid-2025 — nearly triple the 2019 figure, yet far below the dollar’s 48% share. Countries receiving renminbi payments via CIPS face a fundamental limitation. The currency works best in bilateral trade with China. Its utility beyond that corridor shrinks under capital controls and restricted convertibility. Unlike SWIFT — which is currency-agnostic and multilateral — CIPS operates within the boundaries of China’s own financial architecture. Beijing is politically unwilling to fully open that architecture.

Switching costs

Third, switching costs are non-trivial. Institutions migrating to CIPS face infrastructure reconfiguration, compliance recalibration, and counterparty risk adjustments estimated at $10–20 million per institution. For Western-aligned banks, the risks go further. Primary exposure to a PBOC-supervised system carries geopolitical weight — particularly amid US-China tensions over Taiwan and trade. That constitutes an additional deterrent.

The sanctions paradox

The most consequential dynamic may not be CIPS’s absolute scale. It may be SWIFT’s own structural contradictions. Using financial exclusion as a coercive tool has produced a long-term incentive for many actors to reduce their SWIFT exposure. Russia now routes an estimated 20% of its post-sanctions trade through CIPS. Iran, Venezuela, and a range of Belt and Road Initiative partner states have explored renminbi settlement. The reason is simple: dollar-denominated transactions carry the latent risk of exclusion. The 2022 freezing of Russian sovereign reserves held in Western financial institutions reinforced this calculus for central banks globally. It prompted measurable diversification away from dollar-denominated assets.

CIPS’s strategic value to China is therefore less about displacing SWIFT in absolute terms. It is about providing a credible outside option for states at the margins of the dollar-based order. That outside option erodes the coercive power that SWIFT’s network monopoly previously conferred. Even a partial alternative changes the calculus of sanctions policy.

Outlook: fragmentation over displacement in the CIPS vs SWIFT contest

The most plausible trajectory is not a transition from SWIFT to CIPS. It is an increasing segmentation of global financial infrastructure along geopolitical lines. SWIFT retains overwhelming advantages in network scale, institutional trust, and currency breadth. CIPS is growing rapidly. But it remains — and may long remain — a renminbi-centric regional rail rather than a universal alternative. The architecture of the system shifts: away from a single US-anchored network, towards a more fragmented landscape in which multiple rails coexist, each dominant within its sphere of influence.

This fragmentation does not leave the dollar unaffected. The petrodollar system derived much of its self-reinforcing power from the absence of alternatives. As CIPS matures — and particularly if the e-CNY integration and Project mBridge, the multi-CBDC platform involving the central banks of China, Hong Kong, Thailand, the UAE, and Saudi Arabia, expand the system’s multi-currency capacity — the structural demand for dollar liquidity faces incremental but compounding pressure. The battle for financial infrastructure is a battle for the conditions under which future geopolitical leverage is exercised. SWIFT does not need to fall for that battle to matter.

You may also enjoy reading…