Markets do not wait for disruption to become visible before they start pricing it. In energy, finance, and cross-border investment, markets often absorb part of the cost of instability in advance through expectations. This forward-looking element is the geopolitical risk premium: the extra return, spread, or price adjustment that markets demand when political tension raises the perceived likelihood of disruption.

This is not a single official metric published in one place. It is a market effect. Investors, lenders, traders, and firms create it when they attach a cost to the possibility that war, sanctions, coercion, route disruption, or strategic rivalry may alter supply, financing conditions, or expected returns. In that sense, the geopolitical risk premium gives anticipated instability an economic form.

How markets translate tension into cost

Energy markets show this mechanism particularly clearly. Geopolitical shocks affect oil prices through two main channels. The first is macroeconomic: rising tension weakens confidence, investment, and trade, which can reduce demand. The second is risk-based: markets start pricing the possibility of future supply disruption even when current flows remain intact.

For that reason, the relationship between geopolitics and oil prices is never purely mechanical. Not every geopolitical shock pushes prices higher. What matters is the balance markets see between weaker demand and greater supply risk.

The role of strategic chokepoints

This distinction becomes even clearer around strategic chokepoints. The Strait of Hormuz is the clearest example. A very large share of global seaborne oil trade, oil and petroleum product consumption, and liquefied natural gas trade moves through this narrow corridor. Existing alternatives could absorb only part of those volumes if a serious disruption occurred.

In this setting, markets do not price only the commodity itself. They also price the reliability of access to it. Here, the geopolitical risk premium reflects the value markets attach to continuity under conditions of strategic vulnerability.

Beyond oil markets

The same logic extends well beyond energy. Major geopolitical events can widen sovereign risk premiums, weaken equity valuations, and tighten financial conditions. Once markets conclude that conflict or strategic confrontation may damage a country’s fiscal outlook, trade position, or political stability, financing costs begin to rise.

This repricing usually hits more vulnerable economies harder. In those cases, geopolitical stress moves more quickly into borrowing costs and capital allocation. The geopolitical risk premium is therefore not just an oil-market phenomenon. It is a broader repricing of uncertainty across the financial system.

Geopolitical risk and the cost of equity

At this point, the article moves from description to interpretation. A useful analytical approach is to treat the geopolitical risk premium as one possible component of the broader country risk premium that may enter a company’s cost of equity.

The logic is simple. If geopolitical instability makes a country riskier for investors, they demand a higher return. That higher required return can then shape valuation. Under this interpretation, analysts do not need to treat geopolitical risk as a completely separate premium. They can treat it as one of the forces that raises country risk itself, especially when conflict, sanctions, or strategic tension worsen sovereign spreads, financing conditions, capital mobility, or expectations about future cash flows.

The main methodological warning is straightforward. Analysts should not count the same risk twice. If sovereign spreads or CDS-based measures already fully reflect geopolitical stress, they should not add a separate adjustment on top of that.

A broader valuation effect

Seen this way, the link between geopolitical instability and valuation goes well beyond commodity prices. Political and institutional risk can damage the investment environment more broadly. It can weaken policy credibility, worsen financing conditions, reduce capital mobility, and undermine confidence in future cash flows.

The premium is therefore not only about sudden crisis. It is also about the way persistent strategic tension changes the background assumptions on which capital is priced.

Evidence from asset pricing

Academic work on commodity futures supports the term in a stricter asset-pricing sense. Research finds evidence of a measurable geopolitical risk premium across futures returns. Lower-risk contracts tend to outperform higher-risk ones on a risk-adjusted basis, especially during periods of elevated geopolitical stress.

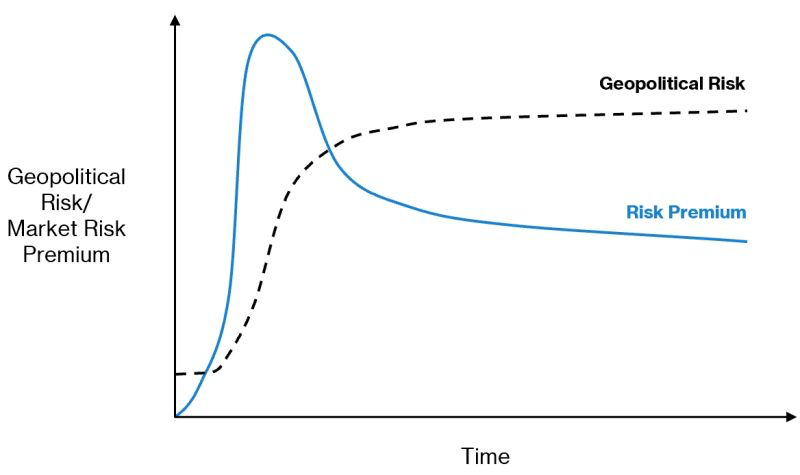

This matters for two reasons. First, it shows that geopolitical exposure is not just a narrative applied after the fact. Second, it shows that this exposure can appear in the structure of returns themselves. Markets often react not only to realised geopolitical events, but also to threats and expectations that come before them. In other words, markets often build the premium before disruption fully materialises.

A premium that can migrate

The concept also has a wider strategic meaning. Geopolitical risk premiums shape not only short-term prices, but also long-term investment choices. Reducing exposure to one vulnerability does not necessarily remove the premium. More often, it shifts the premium elsewhere.

Traditional concerns around oil and gas transit may give way to new dependencies linked to critical minerals, industrial supply chains, or concentrated clean-energy manufacturing. In that sense, the premium can migrate rather than disappear.

Why this matters now

This is why analysts should not treat the geopolitical risk premium as a temporary distortion or a rhetorical flourish. It is the price of anticipated instability. It appears when markets conclude that reliability, continuity, and access can no longer be taken for granted.

In a more fragmented international system, this premium is becoming less episodic and more structural. It is increasingly embedded in energy pricing, sovereign financing, portfolio allocation, and the valuation of resilience itself.

You may also enjoy reading…