The BRI at a crossroads

Belt and Road Initiative debt has become one of the defining fault lines in 21st-century geopolitics. When China launched the BRI in 2013, the ambition was clear. It aimed to replicate the ancient Silk Road — financing infrastructure that would bind Asia, Africa, and Europe into a single commercial network, with Beijing at its centre. More than a decade later, the BRI is the largest infrastructure lending programme in history. Its underlying logic, however, has shifted dramatically. What began as capital export and diplomatic influence is now, in significant part, a sovereign debt management problem. It simultaneously tests China’s role as a creditor power and reshapes the architecture of international finance. It also constitutes a deliberately engineered instrument for renminbi internationalisation.

The scale and structure of BRI lending

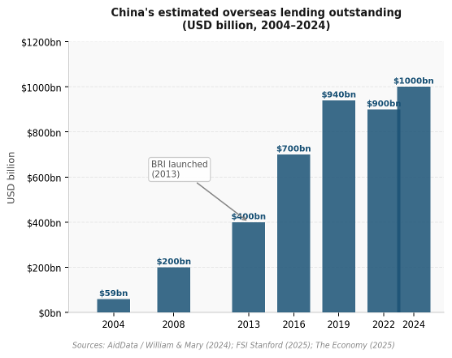

The BRI’s financial footprint is formidable. By 2020, China’s state-owned creditors had issued over $800 billion in loans to more than 150 countries. The principal lenders were the China Development Bank and the Export-Import Bank of China. The vast majority of these loans formed part of the BRI. Total outstanding Chinese overseas debt now exceeds $1 trillion — more than eight times the inflation-adjusted scale of the Marshall Plan. Approximately 150 countries, representing 40% of global GDP, have signed memoranda of understanding formalising their interest in BRI participation.

The structural features of BRI financing distinguish it sharply from multilateral development lending. Loans typically carry commercial or near-commercial rates. They come with short grace periods and non-disclosure clauses. Collateralisation provisions grant Chinese creditors priority over other lenders. Unlike terms from the World Bank or the Asian Development Bank, BRI loans frequently require Chinese contractors and Chinese labour. Procurement must come from Chinese firms. Economic benefits concentrate within China’s supply chain. The debt burden transfers to the recipient sovereign.

The debt distress crisis

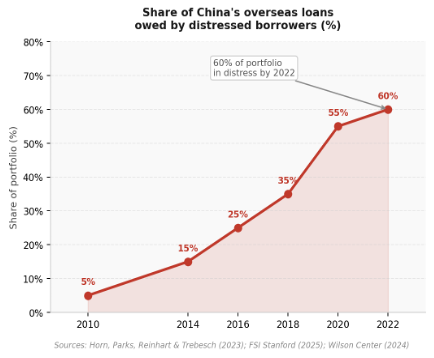

The scale of Chinese overseas lending has grown dramatically since the BRI’s launch. So has the share of that portfolio in distress. Research by Horn, Parks, Reinhart, and Trebesch found that 60% of China’s overseas lending portfolio was owed by distressed borrowers by 2022. That figure stood at just 5% in 2010. AidData’s parallel research corroborates this. 80% of China’s government loans to developing countries have gone to nations in some form of debt distress. More than half of those loans are now in their repayment period.

Case studies in Belt and Road Initiative debt

The case studies are instructive. Sri Lanka’s Hambantota Port was financed by China Exim Bank. It became the archetypal instance of debt-for-asset exchange. Colombo, unable to service its obligations, signed a 99-year lease to a Chinese state firm in 2017. Zambia defaulted in 2020, becoming the first African country to default during the COVID-19 pandemic. China was its largest bilateral creditor. Kenya’s Standard Gauge Railway has been called a “railway to nowhere”. Construction halted mid-route after Chinese funding dried up. Nairobi is now servicing debt on non-operational infrastructure. Indonesia opened debt restructuring talks over the Whoosh high-speed rail project. Costs ballooned from $5.6 billion to $7.4 billion. Annual interest payments alone now reach approximately $120 million. In 2025, developing countries owe China a record $35 billion in annual repayments. $22 billion of that falls on the world’s 75 poorest nations.

China as creditor: outside the Paris Club Framework

The accumulation of sovereign debt distress has placed China in an unprecedented position. It is now the world’s largest official bilateral creditor. Yet it operates almost entirely outside the institutional framework governing sovereign debt restructuring. That framework has existed for nearly seven decades. The Paris Club is an informal group of 22 predominantly Western creditor nations. It has coordinated sovereign debt restructurings since 1956. It works alongside the IMF to impose conditionality, require equal treatment of all creditors, and mandate transparency. China is not a member. It has repeatedly declined to join.

Beijing’s bilateral approach

Beijing’s preferred approach to debt distress is bilateral and sequential. It extends grace periods and rolls over maturities. For strategically significant borrowers, it issues rescue lending through the PBOC’s foreign currency swap lines. This prevents outright default. Horn et al. document that China extended rescue loans totalling over $170 billion between 2000 and 2021. These loans went predominantly to middle-income countries. Default in those countries would most damage Chinese state bank balance sheets. None of these restructurings involved face-value reductions. That is the standard “haircut” in IMF-coordinated workouts. China has also contested the classification of CDB and Exim Bank as official creditors. This excludes the majority of its overseas lending from multilateral restructuring frameworks. The result has stalled the G20 Common Framework repeatedly — in Zambia, Ethiopia, and Sri Lanka alike.

BRI as a Renminbi internationalisation instrument

The debt dimension of Belt and Road Initiative debt tends to dominate Western analysis. The initiative’s currency implications are equally significant. The BRI was conceived in part to expand international renminbi use. It aimed to replicate the connection between resource flows and currency demand that historically underpinned the petrodollar system. The logic is straightforward. If China finances global infrastructure in renminbi and BRI corridor trade settles in renminbi, structural demand for the currency grows independently of market choice.

Evidence of this dynamic is accumulating. By 2024, 40% of Brazil’s trade with China was conducted in renminbi. Just a year earlier, 95% was dollar-denominated. The renminbi’s share in international trade finance reached 7.38% of global transactions by March 2025. It overtook the euro for eight of ten months since June 2024. By October 2025, governments and international bodies had issued ¥68 billion ($9.5 billion) in renminbi-denominated bonds. That is double the total for all of 2024. According to Bruegel, the acceleration from 2022 reflects two factors. First, China’s trade and financing reach in the Global South. Second, the expanding use of US financial sanctions as a coercive instrument.

The limits of Belt and Road Initiative debt diplomacy

Despite these structural advantages, the BRI’s role as a renminbi internationalisation instrument faces significant constraints. Many originate within the initiative’s own lending pathologies. The credibility of an international currency rests on trust. It requires institutional predictability, financial openness, and rule of law from the issuing state. BRI’s track record undermines all three. Opaque loan terms, collateralisation clauses prioritising Chinese creditors, and systematic resistance to coordinated restructuring have reinforced one perception. The renminbi, in many recipient countries’ eyes, operates within a political rather than purely financial logic.

The convertibility contradiction

A deeper structural tension persists. For the renminbi to function as a genuine international currency, it must work beyond bilateral relationships with China. That requires convertibility, deep capital markets, and institutional independence. Yet the conditions making BRI lending politically effective are precisely those impeding full convertibility. State direction of credit, non-disclosure, and the absence of IMF conditionality all constrain the currency’s reach. Beijing cannot simultaneously maximise control over BRI lending and maximise the renminbi’s international utility. As AidData’s Brad Parks has observed, China has transitioned from “the world’s largest official creditor” to “the world’s largest official debt collector”. That reputational shift complicates renminbi adoption outside Beijing’s immediate sphere of influence.

BRI 2.0 and a more cautious creditor

The era of high-risk Belt and Road Initiative debt has, by most accounts, come to a close. Research by Horn et al.indicates that total debt servicing to China’s state banks now exceeds their total new overseas lending. The BRI lending cycle has peaked. Beijing is now primarily in recovery and damage-limitation mode. A rebranded BRI 2.0 emphasises smaller-scale projects, green energy, and digital infrastructure. It applies greater selectivity in choosing sovereign counterparts. It is a model less reliant on debt as the primary instrument of influence.

The renminbi internationalisation agenda, however, is unlikely to abate. The BRI’s trade corridor network continues to expand. CIPS’s settlement infrastructure is growing rapidly. The e-CNY is integrating into cross-border payments. US financial sanctions continue to incentivise dollar alternatives. Together, these forces constitute compounding pressure on dollar hegemony. Not through any single rupture — but through the gradual construction of parallel systems. The central question for the coming decade is whether China can resolve the contradiction between its creditor difficulties and its currency ambitions. Can a state whose Belt and Road Initiative debt is increasingly associated with distress and asymmetric leverage simultaneously build the institutional trust a genuinely international reserve currency requires? That contradiction — not simply the gap in financial market depth — may be the defining constraint on the renminbi’s trajectory.

You may also enjoy reading…