As the 2026 sowing season commences, the blockade of the Strait of Hormuz has transformed the agricultural input market into a battlefield of resource nationalism. Consequently, food security no longer represents a simple trade metric ; it functions as a strategic military lever.

The global squeeze: a two-front war on calories

Geopolitics has finally collided with the periodic table. If the 2022 invasion of Ukraine taught us that we could no longer rely on the global commons to move food, 2026 is teaching us that we can no longer rely on industrial chemistry to create it. We have shifted from a logistical bottleneck in the Black Sea to a molecular blockade in the Persian Gulf. The era of moving calories has ended ; the era of failing to invent them has begun.

The Ukraine prototype : a crisis of circulation

The war in Ukraine served as the first warning. As a global breadbasket, the disruption there caused immediate damage, including blocked ports and charred silos. However, by early 2026, Ukraine has demonstrated “war-hardened” resilience. Remarkably, producers increased agricultural exports by 9.3% as they successfully bypassed traditional chokepoints.

Ultimately, Ukraine taught us that we can re-route logistics. Conversely, the current situation with Iran proves that we cannot re-route chemistry.

The end of the “just-in-time” input era

For decades, global agriculture relied on the “just-in-time” delivery of cheap nitrogen and accessible diesel. Unfortunately, that era ended with the February 2026 airstrikes. Today, the geopolitical risks in the Middle East have shifted. Specifically, the conflict has moved its focus from disrupting fuel for cars to disrupting the biological energy required to feed the planet.

The Iran conflict: the production shock

The nitrogen shield: fertilizer as a weapon of war

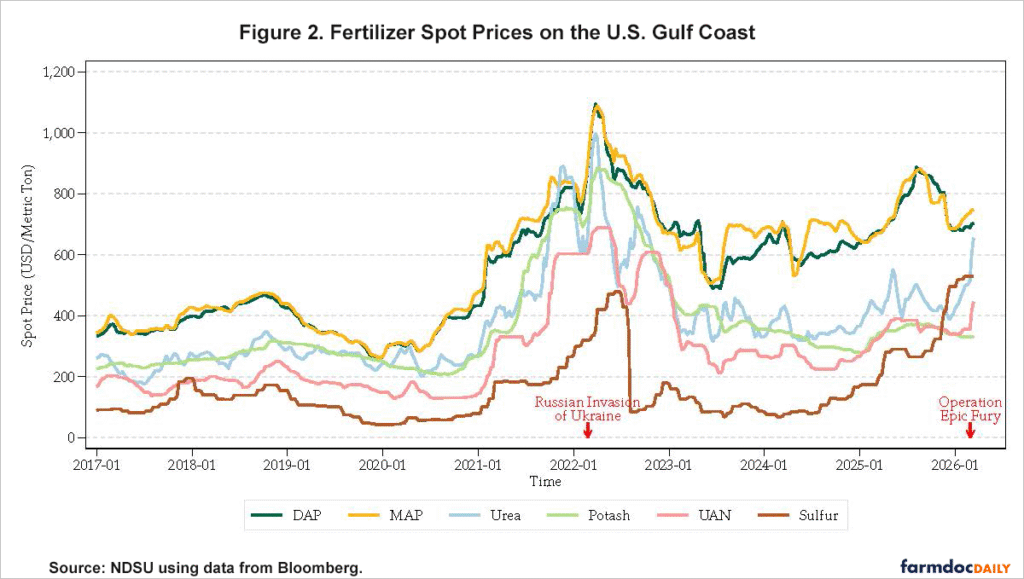

The Strait of Hormuz remains the world’s primary artery for nitrogen-based fertilizers. As a result of the current blockade, the shutdown strands approximately 34% of global urea exports and a significant portion of ammonia.

- Feedstock Sabotage : Natural gas serves as the primary input for nitrogen production. Furthermore, the declaration of Force Majeure by major Gulf gas producers has shuttered fertilizer plants across Southeast Asia and Europe.

- Resource Hoarding : In a move reminiscent of the 2022 supply shocks, China and Russia have suspended all phosphate and ammonium nitrate exports through Q3 2026. Importantly, this is not a simple shortage ; these nations have strategically withdrawn survival assets from the global market.

Consequently, these actions have created a “Nitrogen Shield.” Nations with domestic production now protect their own caloric future, while importing nations face a 50% surge in input costs within a single 30-day window. Moreover, unlike grain, which allows for storage, nitrogen requires application within a narrow window. If a farmer misses the April sowing window, the crop fails regardless of future price corrections.

The diesel divide: distribution failures at the last mile

While crude oil prices dominate the news, the agricultural crisis, in reality, constitutes a diesel crisis. Farming relies heavily on diesel and the distribution network is currently failing.

According to the IEA’s latest market report, refined product shortages hit “the last mile” hardest. Specifically, in the Midwest and Western Europe, authorities are rationing diesel for spring operations. As a result, farmers who did not secure physical reserves in Q4 2025 now face prices exceeding $4.80 per gallon : a cost that makes many high-intensity crops a form of financial suicide.

The 2026 acreage flip: hedging against scarcity

The geopolitics of the Persian Gulf currently dictate the crop maps of the American Midwest and the Brazilian Cerrado.

| Factor | Strategic Shift | Economic Impact |

| Nitrogen Cost | +40-50% since Feb 2026 | Forced shift from corn to soybeans |

| Diesel Access | Rationing in SE Asia/EU | Idled machinery & “Last Mile” failure |

| Yield Outlook | 5-7% global maize drop | Imminent price spike in Q4 2026 |

In essence, farmers no longer make agronomic decisions ; they make energy-hedging decisions. The move to less input-intensive crops like soybeans serves as a survival tactic. Nevertheless, this shift creates a massive global caloric deficit for 2027.

Strategic outlook: securing input sovereignty

The current strategy of “waiting for prices to drop” represents a fundamental misunderstanding of the current conflict. On the contrary, we have entered a period of agricultural deglobalization. Markets no longer measure the opportunity cost of delaying sowing in reduced margins. Instead, producers now measure it by the potential loss of the land itself.

Ultimately, the “new geopolitics of agriculture” dictates that the fertilizer plant now holds more strategic value than the oil refinery. Those who fail to secure input sovereignty by the end of this sowing window will find themselves at the mercy of a global market that no longer seeks to feed the highest bidder, but only to feed itself.

Further perspective

For a broader discussion on the geopolitical and regulatory forces shaping global food markets, this interview offers additional context : Who Controls Food Markets? Geopolitics and Regulatory Power

References:

- The Weaponization of Chokepoints: 2026 Outlook

- Why Qatar’s Force Majeure is the Real Food Crisis

- The Diesel Divide: Who Survived the Spring Sowing?

- Strait of Hormuz Closure and Fertilizer Supply Risks for U.S. Agriculture

You may also enjoy reading…